Understanding Green, Social and Sustainability Bonds

Green bonds and other debt instruments geared toward sustainability are becoming an important part of global fixed income markets. More and more, investors look to align their portfolios with their financial goals and internationally recognized sustainability goals such as The Paris Agreement or UN Sustainable Development Goals (SDG).

So what are green bonds? And how do they relate to – and differ from – social, sustainability and sustainability-linked bonds?

First, it’s important to distinguish between use of proceeds bonds and sustainability-linked bonds.

- Use of proceeds bonds, as the name suggests, fund projects with dedicated environmental and/or social benefits.

- Sustainability-linked bonds do not finance particular projects but rather finance the general functioning of an issuer that has explicit sustainability targets that are linked to the financing conditions of the bond.

Green Bonds

Use of proceeds

These bonds are devoted to financing new and existing projects or activities with positive environmental impacts. We believe impactful green bonds should be issued in line with the Green Bond Principles (GBP) from the International Capital Market Association (ICMA), a set of voluntary guidelines that promote more transparent, unified reporting on bonds’ environmental objectives and estimated impact. In fact, ICMA is relevant for green, social or sustainability-linked bonds, since ICMA provides guidelines for all forms of such bonds.

Examples of project categories eligible for green bond issuance include: renewable energy, energy efficiency, clean transportation, green buildings, wastewater management and climate change adaption.

Social Bonds

Use of proceeds

To qualify as a social bond, the proceeds must finance or refinance social projects or activities that achieve positive social outcomes and/or address a social issue. In many cases, social projects are aimed at target populations such as those living below the poverty line, marginalized communities, migrants, unemployed, women and/or sexual and gender minorities, people with disabilities, and displaced persons.

Similar to green bonds, issuance of social bonds is oriented by a set of voluntary guidelines – in this case the Social Bond Principles (SBP) from ICMA – aimed toward improved disclosure and transparency in the social bond market. The SBP outline best practices for issuing a social bond; they also arm investors with the information necessary to evaluate the social impact of their investments.

Recently, we have seen a new type of social bond emerge in the form of COVID-related bonds. These bonds have use of proceeds specifically aimed at mitigating COVID-19-related social issues and are particularly focused on the populations most impacted.

Examples of project categories eligible for social bonds include: food security and sustainable food systems, socioeconomic advancement, affordable housing, access to essential services, and affordable basic infrastructure. Social projects can include related and supporting expenditures such as research and development and, in situations where projects also have environmental benefits, issuers may determine classification as a social bond based on the primary objective of the underlying project.

Sustainability Bonds

Use of proceeds

Sustainability bonds are issues where proceeds are used to finance or re-finance a combination of green and social projects or activities. These bonds can be issued by companies, governments and municipalities, as well as for assets and projects and should follow the Sustainability Bond Guidelines from ICMA, which are aligned with both the GBP and SBP. They can be unsecured, backed by the creditworthiness of the corporate or government issuer, or secured with collateral on a specific asset.

Examples of project categories eligible for sustainability bonds include those in the green and social bonds categories.

Sustainability-linked Bonds

Sustainability-linked Bonds –such as key performance indicator (KPI)-linked or SDG-linked Bonds – are structurally linked to the issuer’s achievement of climate or broader SDG goals, such as through a covenant linking the coupon of a bond. In this case, progress, or lack thereof, toward the SDGs or selected KPIs then results in a decrease or increase in the instrument’s coupon. These bonds can play a key role in encouraging companies to make sustainability commitments at the corporate level, particularly through aligning to the UN SDGs or Paris Agreement.

Source: ICMA

History of Green Bonds:

In 2007, the U.N. Intergovernmental Panel for Climate Change published a report linking human action to global warming, which added further weight to the growing body of data. Recognizing the risk posed by climate change as called out by the report, institutions (i.e., Swedish pension funds and their bank, SEB), the World Bank, and climate change experts (i.e., CICERO, the Centre for International Climate and Environmental Research) collaborated to establish a process for debt markets to be part of the solution. To ensure investment and capital-raising for sustainability projects materially advanced positive environmental outcomes, a set of eligibility criteria was determined. And, in 2007-2008, the European Investment Bank and the World Bank successfully issued the first green bonds.

The first green bond acted as a framework for the entire green bond market by creating criteria for issuance and reporting, as well as setting a precedent for the use of external reviews by including CICERO as a second opinion. Building on the first green bond issuance, ICMA established the GBP to further develop transparent guidelines for investors to support climate solutions. ICMA typically updates the GBPs on an annual basis and has also instituted voluntary guidelines for social bond, sustainability bond and sustainability-linked bond issuance.

Source: The World Bank

Looking to the Future:

While the explosive growth in green bond markets is encouraging, we believe the opportunity set for climate action within the bond universe is even larger. For those specifically looking to invest in climate solutions, it’s important to understand that the growing climate bond market includes not just labeled green bonds, but also unlabeled green bonds, and the bonds of climate leaders:

- Green bonds are debt securities issued explicitly for environmental or climate-related projects, as detailed above.

- Unlabeled green bonds are debt securities of issuers fundamentally aligned to low carbon products and services, such as a renewable energy company or a municipal water system improvement bond, rather than a certified green bond.

- Bonds of climate leaders, as we define them, are debt securities of issuers we deem to be at the forefront of the net-zero carbon transition, leading their industries forward. These issuers have demonstrated a commitment to mitigating carbon emissions and their broader environmental impact in sectors that may involve water, plastic, air pollution or biodiversity.

Why invest in Sustainable (Green, Social, Sustainability and Sustainability-linked) Bonds?

Sustainable bonds, which include green, social, sustainability and sustainability-linked bonds, can offer a range of potential benefits including:

- Mitigating physical, transition, and long-term sustainability risk and seizing potential opportunities: The long-term challenge of decarbonizing the economy in a socially equitable way comes with risks, but it also offers opportunities for active investors. We recognize that ESG factors are increasingly essential inputs when evaluating global economies, markets, industries and business models. Material ESG factors are also important considerations when evaluating long-term investment opportunities and risks for all asset classes, public and private markets.

- Meeting investor demand: Sustainable bond issuance is rising, regulations are setting global standards, client interest in ESG practices is increasing and, most importantly, responsible investing is becoming more mainstream. We expect that the COVID-19 crisis could cause even more investors to look for sustainable investment choices, and we have observed growing issuance in social, SDG, and specifically pandemic-related bonds on top of a growing green bond market. Focusing on sustainability supports growth over the medium and long term in an inclusive way.

- Aligning with sustainability goals: Sustainable bonds provide investors with a means of aligning their asset allocations with sustainability objectives in a meaningful way. We believe fixed income is an important asset class to drive material ESG change. The global bond market is almost double the size of the equity market and, unlike equity securities, which are in perpetuity, bonds mature, prompting companies to return to the market to refinance. By engaging with companies when they need to fundraise, investors can help push for sustainability commitments or specific sustainable issuance, and accelerate positive social and environmental change.

What are the challenges?

While the establishment of the guiding principles has reinforced the integrity of the sustainable bond market, the act of “greenwashing,” or issuers misrepresenting the positive environmental impact of bond proceeds, is an ongoing challenge investors may face. Greenwashing can occur due to the relatively broad criteria for what constitutes a green bond and lack of formal issuance guidelines in many emerging markets. These challenges emphasize the importance of an investment manager that carefully assesses security documentations to determine the underlying use of proceeds and the expected impact.

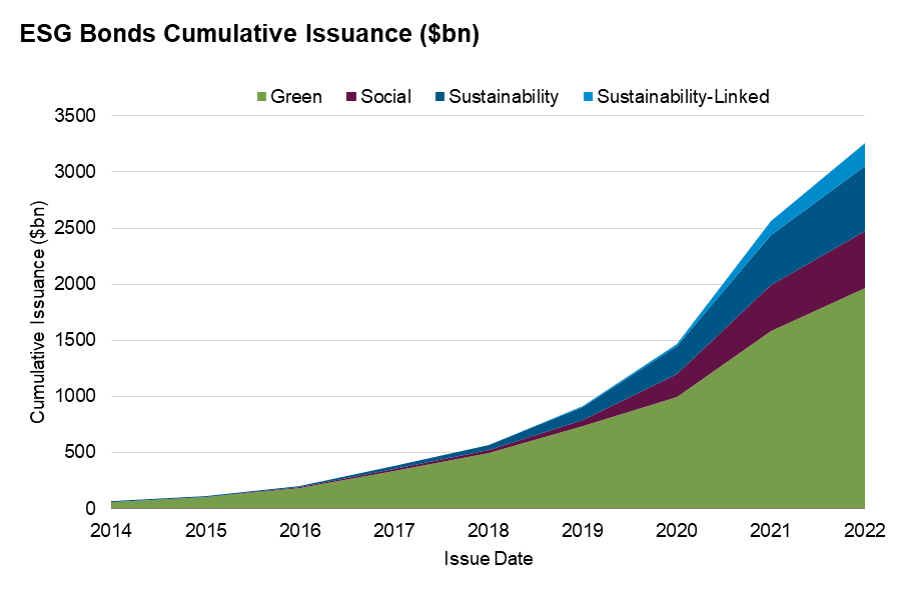

Issuance in the ESG bond space has grown over the years, with total cumulative issuance passing the $3 trillion mark as of 30 September 2022

Source: Bloomberg

As the growing sustainable bond market still represents only a fraction of the broader fixed income market, these investments may carry more liquidity risks and overconcentration risks to certain issuers, sectors or regions. However, sophisticated investment managers are equipped to effectively manage these risks and to target attractive risk-adjusted returns.

In addition, sustainable bonds, like any other fixed income instrument, have credit or default risk – the risk that the borrower fails to repay the loan and defaults on its obligation. The level of default risk varies based on the underlying credit quality of the issuer.

To learn more about how we look to find the likely “winners” of the transition to an SDG-aligned and net zero carbon economy, please see PIMCO’s ESG insights.

Find sustainable fixed income strategies with PIMCO’s range of ESG investing funds.

Disclosures

Environmental (“E”) factors can include matters such as climate change, pollution, waste, and how an issuer protects and/or conserves natural resources. Social (“S”) factors can include how an issuer manages its relationships with individuals, such as its employees, stakeholders, customers and its community. Governance (“G”) factors can include how an issuer operates, such as its leadership, pay and incentive structures, internal controls, and the rights of equity and debt holders.

PIMCO is committed to the integration of Environmental, Social and Governance (""ESG"") factors into our broad research process and engaging with issuers on sustainability factors and our climate change investment analysis. At PIMCO, we define ESG integration as the consistent consideration of material ESG factors into our investment research process, which may include, but are not limited to, climate change risks, diversity, inclusion and social equality, regulatory risks, human capital management, and others. Further information is available in PIMCO’s Environmental, Social and Governance (ESG) Investment Policy Statement.

A word about risk: All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. ESG investing is qualitative and subjective by nature, and there is no guarantee that the factors utilized by PIMCO or any judgment exercised by PIMCO will reflect the opinions of any particular investor, and the factors utilized by PIMCO may differ from the factors that any particular investor considers relevant in evaluating an issuer’s ESG practices. In evaluating an issuer, PIMCO is dependent upon information and data obtained through voluntary or third-party reporting that may be incomplete, inaccurate or unavailable, or present conflicting information and data with respect to an issuer, which in each case could cause PIMCO to incorrectly assess an issuer’s business practices with respect to its ESG practices. Socially responsible norms differ by region, and an issuer’s ESG practices or PIMCO’s assessment of an issuer’s ESG practices may change over time. There is no standardized industry definition or certification for certain ESG categories, for example “green bonds”; as such, the inclusion of securities in these statistics involves PIMCO’s subjectivity and discretion. There is no assurance that the ESG investing strategy or techniques employed will be successful. Past performance is not a guarantee or reliable indicator of future results.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2022, PIMCO.

CMR2022-1020-2520209